010-80850896;13001093985

010-80850896;13001093985

010-80850896;13001093985

010-80850896;13001093985

BEIJING, July 18 (TMTPOST) -- Some clients of five village and township banks are receiving money from regulatory authorities in central China after fighting to defeeze their accounts over months.

Statements of provincial financial regulators came last Monday, one day after a massive protest in central China’s Henan province. The first “advance payments,” a term which provincial authorities used to refer to the return of frozen funds, have been sent to individuals with a combined asset of no more than 50,000 yuan ($7,400) at a single bank since last Friday. The remaining clients with assets of over 50,000 yuan have to await further notice.

Even those who qualify for a return of their funds still had to wait following an online system crash last Friday due to surging traffic.

“As depositors, we used to be treated by the banks as kings, but now we ended up like beggars!” one customer posted on Chinese social media.

A GATHERING STORM

In April, many customers across China found that they were unable to withdraw their money from four local banks headquartered in central China’s Henan province and one in Anhui province. Their alleged deposits at Yuzhou Xin Min Sheng Village Bank, Shangcai Huimin County Bank, Zhecheng Huanghuai Community Bank, New Oriental Country Bank of Kaifeng and Guzhen Xinhuaihe Village Bank have been frozen. The amount of money or the number of customers affected have not been confirmed by the authorities. An estimate of 400,000 people with 40 billion yuan ($6 billion) were involved, according to Sanlian Lifeweek, a Chinese magazine.

Victims started gathering in front of those banks in April and May, demanding the return of their life savings. However, in June, many were stopped at the border of Henan province, as their COVID-19 quick response (QR) health codes had turned red. Other bank customers also found their QR codes red even if they had never been to Henan province or attended such gatherings. Heated discussions went on about a suspected abuse of China’s COVID-19 health code system, which was introduced in Feb. 2020 to detect potential contact with confirmed COVID-19 cases and limit the spread. Once the code was flagged red, users were required to start quarantine immediately as they have a confirmed or potential risk of infection.

A few local officials were later punished for giving 1,317 bank customers a red QR code improperly. However, such punishment failed to stem the growing frustration, as bank customers still didn’t get their money back. Protests continued in early July, as investigations into the scandal went under way.

A CRIME UNDETECTED FOR LONG

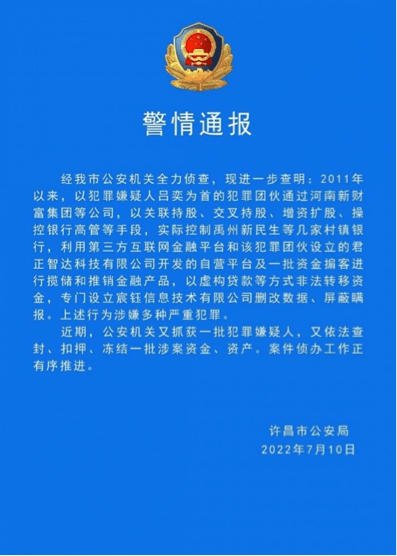

Local police announced on July 10, since 2011, a criminal group led by Lu Yi has controlled the rural banks in Henan province, by engaging in related party transaction, cross ownership, capital increase and share expansion, and the manipulation or embezzlement by bank executives through companies, including Henan New Fortune Group.

Xuchang police in Henan province announced the arrest of a number of suspects who allegedly had used the rural banks to solicit public funds illegally since 2011.

And they used third-party fintech platforms, a self-owned platform and investment brokers to solicit depoll financial products illegally and siphon off money. They even set up a company which deleted and modified data to cover up their crimes.

Although police forces have arrested several suspects, the statement didn’t mention if the mastermind of the crime was among them.

Henan Police accused a number of suspects, whom have been arrested, of using the rural banks to solicit public funds illegally since 2011.

DEPOSITS OR INVESTMENT PRODUCTS?

One day after the announcement, local authorities unveiled the payment plan, which came into effect last Friday. Clients qualified as the first batch of recipients needed to fill out an online form before using a mini program on WeChat, China’s largest messaging service, to get advance payment.

A bank customer shared on Chinese social media that the payment was received Friday.

However, many were not favored by fortunes. They got stuck in the process for various reasons, including inaccessibility to customer services, display of an incorrect amount of money and facial recognition failure.

“It’s just too hard. I spent the whole day doing nothing else but trying to withdraw my money. It turned out I couldn’t even get my information properly registered,” one client said on social media.

Apart from them, clients who were not among the first batch also worried if their money could be fully returned.

The answer lies in who is paying the price.

The advance payment comes from the proceedings from disposing some of the assets that the local police have sealed up, distrained, and frozen involved in the case, according to China Central Television Business Channel, a state-owned media outlet. And an organization named Henan Province Rural Credit Cooperatives Joint Agency was responsible for carrying out this payment plan.

Uncertainty remains whether the proceedings from the sezied assets should pay all of the clients of the embattled banks.

Thus, whether the bank clients’ frozen funds are deposits matters significantly in this case. In China, deposits in domestic banks are covered by insurance. According to the Deposit Insurance Regulation, each depositor is promised up to 500,000 yuan ($73,998) per bank. However, the announcement released on Monday contained a coined term - “off-statement sheet businesses” - to describe the activities. This term distingushes the funds that were accurately accounted by the banks and reported to regulators and those handled improperly by the distressed rural banks.

“This word is unlike the common term off-balance sheet financing, an accounting practice that allows companies to keep certain liabilities off their balance sheets. It’s carefully chosen to bypass the idea of balance sheets,”said financial regulation analyst Sun Haibo.

The police statement made it more clear that such frozen funds included deposits and financial products.

“If the funds of the bank clients are deposits, they are protected by the deposit insurance scheme,” said Wang Deyi, lawyer and founder of BeiJing XunZhen Law Firm. “However, if liable parties are suspected of committing a crime, the process of investigations, trials, recovery and return of stolen money can be very long. And given that a considerable part of the money will be transferred, victims wouldn’t be compensated too much,” he added.

The payment came in as “advance payment,” which is carried out by a provincial joint agency as a temporary solution. Unlike the coverage of deposit insurance, it is not mandatory.

Despite all these uncertainties, the good news was that at least all the bank clients with a frozen account of less than 50,000 yuan, no matter it was deposits or financial products, were guaranteed to get all their money back.

RISKS OF SMALL BANKS

Although all of the banks involved in the current withdrawal incident were village and township banks, they are legitimate financial institutions that have had a positive impact on rural economy over the years. In December 2006, China Banking Regulatory Commission introduced a policy that encourages the creation of township and village banks, a new type of banks in China, in order to provide more convenient finanical services to farmers.

However, given rural banks are usually located in less-developed regions, regulatory oversight of them can be insufficient. Coupled with their small size, that loophole gave rise to the abuse of power by some wayward shareholders.

In recent years, rural banks have partnered with online platforms to reach more clients, including those from urban regions or other provinces, snowballing potential risks. According to Sanlian Lifeweek, most of the clients involved in the incident were online customers using accounts on third-party internet platforms. A recent change on such accounts on Du Xiaoman Financial, China’s tech giant Baidu’s fintech arm, fuelled concerns. Some clients alleged the category of their funds was misclassfied as financial products, rather than deposits. Since only deposits are protected by the deposit insurance program, they worried that that the change in the nature of their funds would cost their life savings. Du Xiaoman later clarified that it was just a misunderstanding.

In the meantime, Chinese regulators have tightened supervision of such small lenders. Last year, commercial banks were reminded to operate deposit businesses in compliance with laws and regulations, when using internet platforms. In another announcement, banking regulators emphasized village and township banks could only act as sales agencies that sell financial products of wealth management companies, instead of selling products of their own.

“This whole withdrawal crisis has shattered my world. The people who put their money into rural banks are the ones entrusting such institutions with their life savings, including my grandma. The fact that they were truly hard-earned money made me feel so sad, and so hard to believe it,” one social media user posted. “I hope this crisis can be resolved properly. Otherwise, once the public lost confidence in the banking system, I couldn’t imagine what would happen next.”

Numerous netizens expressed their concerns over the financial stability. By releasing the advance payment plan, regulators were also trying to tamp down the negative impact. Village and township banks, with the shortest history as a bank category, are relatively insignificant by assets to China's overall banking system, which consists of five major state-owned banks, joint-stock commercial banks, urban commerical banks and rural commercial banks.

扫一扫了解更多

扫一扫了解更多 扫一扫了解更多

扫一扫了解更多COPYRIGHT©2022ALL RIHGTS RESERVED 北京寻真律师事务所 版权所有 京ICP备2022011643号